Loan commitment is neither a moat nor validation, and seeing why takes reading what the company won't show you.

Introduction

Before you continue, please search for "Phoenix Tailings" in the LinkedIn search bar and look at the recent posts mentioning the Office of Strategic Capital. Some numbers claim one billion dollars, even 1.2 billion dollars, and a 500 million dollar loan. If you notice, the tone in every post is positive. But what is the real number here? If you compete with them, does it make you worry? And if you want to invest in them, does this encourage you or not?

It's neither a moat nor validation, and seeing why takes reading what the company won't show you.

$1 billion, $500 million, or $1.2 billion

It's a $500 million conditional loan, funded by the federal government of the USA. Since Phoenix Tailings is a private company, we cannot see what conditions beyond generic financial and technical due diligence they have to fulfil. But there are small windows into their world we can take a look. A federal loan signals validation and a moat, but is it the case? It depends on who funds it and how they fund it.

Who funds

Capital-intensive startups usually die before scale-up. The industry term for the demise of startups is the valley of death. In 2022, the U.S. Department of Defense (DoD) finally decided to help some startups that are vital to national security pass this valley of death. Therefore, they created the Office of Strategic Capital (OSC). It's the DoW's investing arm. There's a lot to say about this Office, but in short, they mimic the venture capital style of funding. OSC has the same role for DoW as In-Q-Tel does for the CIA.

It means they fund companies that are commercially viable and critical to national security.

Who gives them the authority

The National Defense Authorization Act. The act is quite long, but the relevant part to the recent news is the composition of the loan. 80% of the capital should come from the non-federal sector. It's a form of blended finance, with the majority held by private investors.

The statute introduced three different instruments: loan guarantees, direct loans, and technical assistance. The OSC, in its announcement, stated "Conditional Loan Commitment." So, if Phoenix Tailings successfully passes the due diligence, it will receive a $500 million direct loan.

The Act seems to provide capital, but in many ways it constrains the future capital flow. The source of private capital matters to OSC; non-adversarial ownership or equity is an absolute must.

Signal

The most important signal the loan tells us is about the conversion of Phoenix Tailings from 200 tons a year into probably thousands of tons a year. A new facility called Freedom. A fully integrated domestic rare earth separation and metallization platform built to secure a critical supply chain in the U.S.

The loan at this stage is just a promise, but it doesn't add anything to the moat of Phoenix Tailings. If the price of REEs remains high with enough demand, this non-dilutive capital will hedge against the competitors in the future.

The Risk Part 1

Does this loan bring any risk to Phoenix Tailings?

Yes. The loan is a cost with a premium that they have to pay back. So if the demand softens, or the price of the REEs falls way below the current price of $50-60/kg, they might struggle to pay back. The loan itself is very flexible; to mitigate this risk, it allows deferred payment for years.

And there are competitors. One of them is MP Materials, an indirect competitor. They have already secured floor pricing. Phoenix Tailings hasn't secured any floor pricing yet. This floor guarantees a 10-year price floor of US$110 per kilogram for neodymium and praseodymium (NdPr). To hedge against this, Phoenix Tailings' architecture by design allows them to separate a basket of products, so they remain less vulnerable to a single commodity pricing. But they remain vulnerable to China's price manipulation. Phoenix Tailings is a price taker. Phoenix's only real floor is its cost sheet. If its process runs cheaper than the China-suppressed price, it survives a price war without a contract. That's the moat doing the work the loan can't verify now.

Why this specific Loan matters

This seems like a simple loan. Why does it matter? Phoenix is private. There is no 10-K or investor deck; we cannot look into their cap table without paying $25 000 subscription fees. So, how do you read a company that shows you nothing? You read the paper, the loan drags into daylight: the statute that sets the rules and the eligibility bar OSC made them clear, and the filings of Energy Fuels, a public company that took the same loan the same week, whose disclosures stand in for the terms Phoenix won't show.

What OSC Doesn’t Want?

Private investors are concerned about the ability of the company to generate revenue. How do they do due diligence? The best option is a credible third-party entity. OSC renders companies ineligible for a loan:

If the prospective borrower is seeking financing for a project or transaction to produce a technology, product, asset, and/or service for which the Federal Government is the sole user.

If the prospective borrower is seeking financing for a project or transaction to produce a technology, product, asset, and/or service where repayment is majority dependent on current or anticipated Federal sources (e.g., grants or contracts).

OSC verifies the ability of Phoenix Tailings to generate enough revenue to pay back the $500m loan plus interest. But OSC is legally barred from being Phoenix's customer. This is in contrast with Phoenix Tailings' marketing. The entire philosophy of Phoenix Tailings is domestic feedstock and domestic production to supply defense REE demand. It means Phoenix Tailings' private market should be very large. Take note, competitors: if they get the loan, you'll be competing with them neck and neck while they enjoy a $500m non-dilutive flexible loan. This matters even more when China artificially keeps the prices low, or demand softens. They’ll have a financial edge you might not have.

If the conditions are met, it also reliefs the investors of who will fund the rest of the project. For VCs, it’s a guaranteed partner.

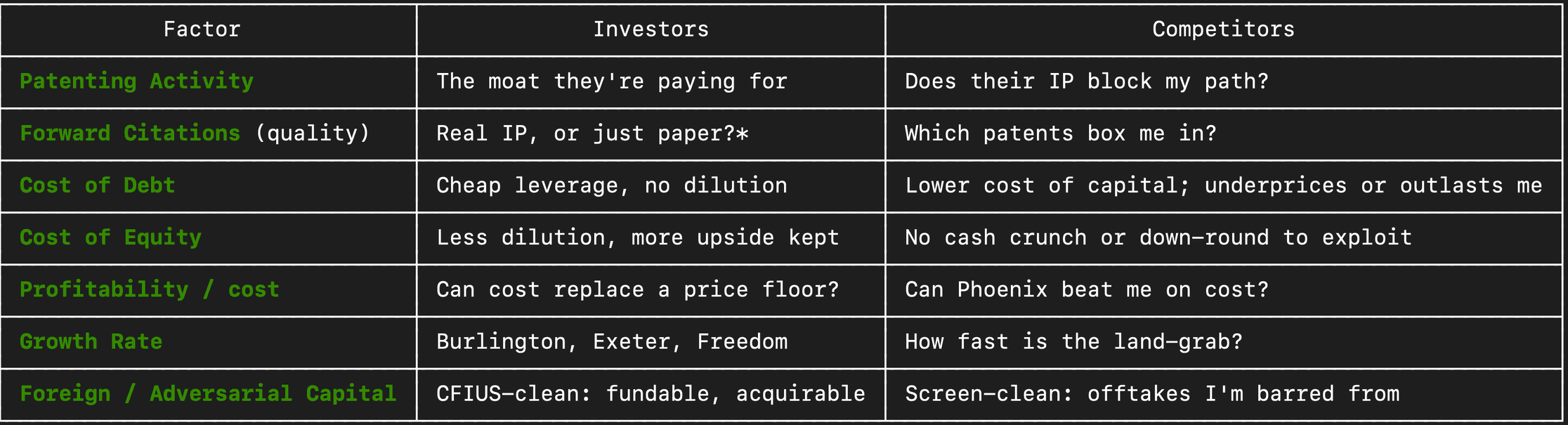

Does OSC care about the competitiveness of Companies?

OSC has a rigorous framework to evaluate the competitiveness of the companies it invests in. The relevant variables for competitors are:

OSC Framework

*Citations lag 2–5 years, so on Phoenix's young patents the metric reads near-zero for reasons unrelated to quality

The Twine - Risk Part 2

In the same week, OSC announced the same type of loan to Energy Fuels. The amount is $725 million, combined with $500m for Phoenix Tailings sums up to $1.25B, which is probably the source of confusion for some people who announce Phoenix Tailings' $1.2B funding.

But Energy Fuels is a public company; they disclose more information on their filings. The most important information we find is this: for Energy Fuels, this is senior debt. It has absolute priority over private capital.

It's the same type of loan, in the same week. Although we cannot say with 100% certainty that Phoenix Tailings gets the same deal, the probability is high. This matters a lot to private investors. In a downturn, the government stands ahead of the people who funded the company.

Conclusion

The loan will hedge against the competitors in the future, it makes their fundraising slightly easier if they go to the Series C and beyond. It doesn’t expand the moat or add any layer to it. The loan is quite neutral in the long-term since it doesn't secure any floor-pricing or off-take agreement and put some constraints on the future capital flow from certain private capital flow.

Any time the government touches a private company, the money leaves a trail it can't control and that trail is readable. That's the work: finding what a private company can't hide.

References

DOD commits $1.2B in conditional loans to Phoenix Tailings, Energy Fuels. (2026). Manufacturing Dive. https://www.manufacturingdive.com/news/defense-energy-fuel-phoenix-tailings-loans-war-dod-office-strategic-capital/823331/

Energy Fuels Inc. (2026, June 18). Energy Fuels receives conditional U.S. government support [Press release]. SEDAR+. https://www.sedarplus.ca/csa-party/records/document.html?id=81c0cbe205406c96888a06cde6d4958b7878bcf8c41571b4cdff6ebb65867f0b

Energy Fuels Inc. (2026, June 23). Energy Fuels announces definitive agreement to acquire VAC for $1.9 billion [Press release]. SEDAR+. https://www.sedarplus.ca/csa-party/records/document.html?id=c99ec4e24e08728d2fce274fa047c6427d430ca96c508e41dcee819c6f79518f

Morgan Lewis. (2025, January). DoD opens loan applications for $1 billion in funding for critical technologies. https://www.morganlewis.com/pubs/2025/01/dod-opens-loan-applications-for-1-billion-in-funding-for-critical-technologies

National Defense Authorization Act for Fiscal Year 2024, Pub. L. No. 118-31, § 903, 137 Stat. 136 (2023) (codified at 10 U.S.C. § 149). https://www.congress.gov/bill/118th-congress/house-bill/2670/text

Office of Strategic Capital. (n.d.). OSC credit program: Debt financing. U.S. Department of War. Retrieved June 27, 2026, from https://www.cto.mil/osc/credit-program/

Office of Strategic Capital. (n.d.). OSC investment fund financing: CTLP program and SBICCT initiative. U.S. Department of War. https://www.cto.mil/osc/sbicct-initiative/

Office of Strategic Capital. (2024). OSC credit program FAQs (Publication version) [Fact sheet]. U.S. Department of War. https://www.cto.mil/wp-content/uploads/2024/10/OSC-Credit-Program-FAQs_Publication-Version.pdf

Office of Strategic Capital. (2026, June 16). Office of Strategic Capital signs $500 million conditional loan commitment with Phoenix Tailings [Press release]. U.S. Department of War. https://www.war.gov/News/Releases/Release/Article/4517853/

Office of Strategic Capital. (2026). Conditional loan commitments: Energy Fuels (US$725 million) and Vulcan Elements & ReElement Technologies (US$700 million) [Press releases]. U.S. Department of War. https://www.war.gov/News/Releases/Release/Article/4520819/; https://www.war.gov/News/Releases/Release/Article/4339788/