If you starve the rest, you'd better take their possession.

It started in 2010. A company called Computational Geosciences was processing geophysical data with code nobody had thought to call machine learning yet.

Then the standalone players arrived. Earth AI in 2017 and KoBold Metals behind it. At first, they all looked the same. But then the paths split. KoBold found a copper deposit in Zambia and kept the ground. In Australia, OreFox found ground too, and sold it off for shares. Datarock got swallowed by IMDEX, and Minerva Intelligence became a different platform.

In just two years from 2024, everyone will be equally capable. And the world restructured into four segments.

They knew it on Sand Hill Road better than everyone: It was only a matter of time until everyone else caught up with AI in mining. Machine learning and AI improve too fast. So venture capitalists had to peg the return model to something else, and the business model was a means to get there. This is a narrow perspective of who survives when everyone is equally capable. The new competition.

Before 2016, there were few companies with a dedicated machine learning department, and even fewer integrated ML into their commercial program. Computational Geosciences Inc., now 94%-owned by Ivanhoe Electric, was integrating ML into commercial mineral exploration as early as 2010.

It is quite hard to find out what counted as AI/ML, since the vocabulary from the early 2000s up to 2023 was very fuzzy. I found “sophisticated code” was the closest thing to ML in public filings. From 2016, we see standalone companies describe ML/AI as the core of their business. In 2026, we have the full spectrum of business models.

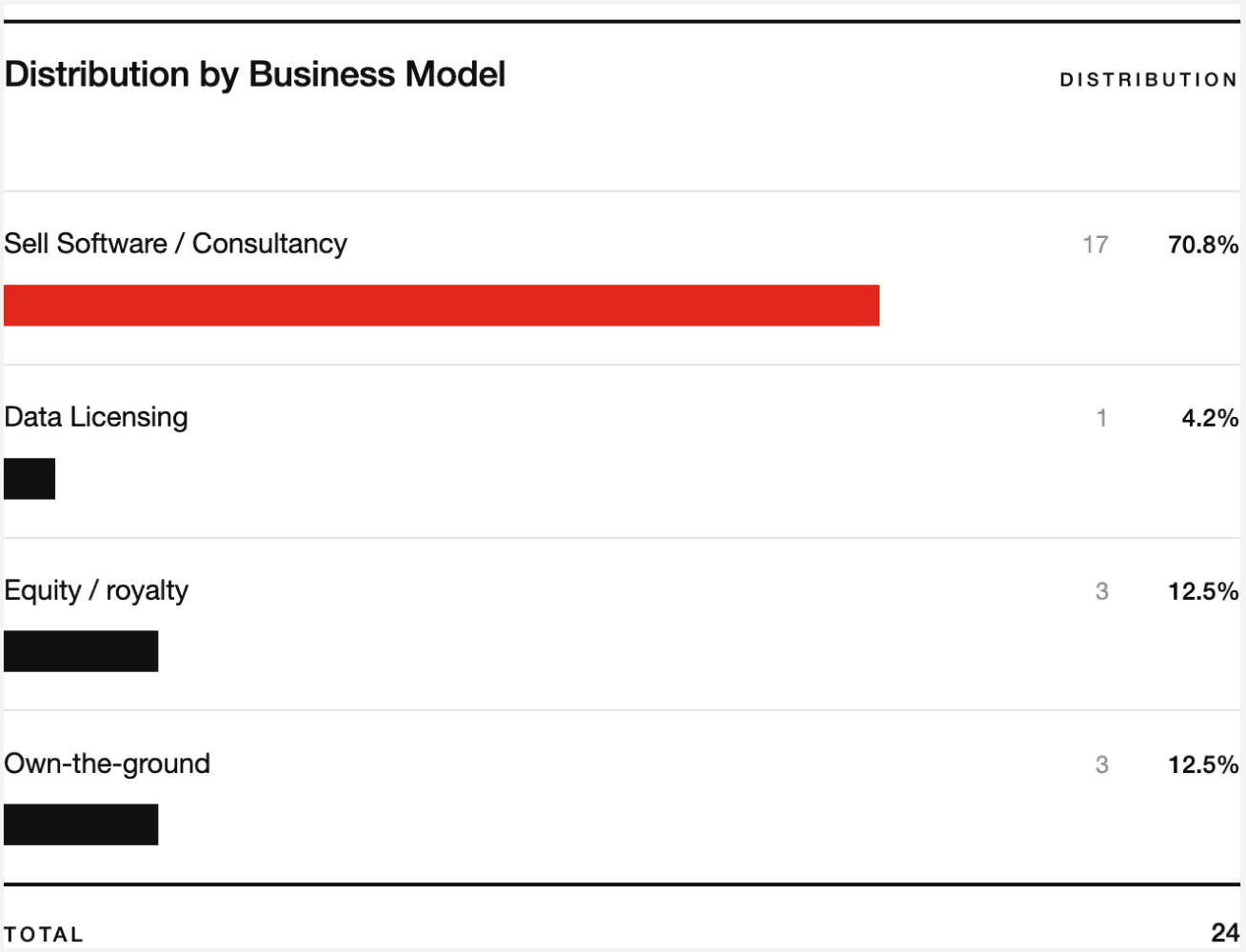

Who Owns What?

The majority, around 71% of these companies(Group 1), process public data and private clients' data; they own nothing besides the algorithm.

The group above them generates data through custom-made hardware and processes it through their software. They also own nothing. In 2026, there is only a single company doing drone survey and in-site data generation via sensors, but the scope is limited to conventional methods.

The smart ones process public and private data, but they cut a small slice in the form of a royalty or net smelter return.

And the rest take the ground and process all sorts of data. They take full or minority ownership (up to 49%) in the mine

Distribution of Business Models

Why are most of these companies in the first group?

Because they don't finance themselves but they dilute with private funds. And private investors need a clear risk profile to invest, something clear enough to model. The first group is the only one that allows them to do so. Remember, almost all of these companies are backed by venture capital, or an active mining company.

False Negatives Are Invisible

For the software and consultancy companies, the risk is capped at a false positive: the AI points to ground that turns out to hold no deposit. That sounds risky until you compare it to targeting without AI. Instead of narrowing the ground with software, you narrow it some other way, and either way, you still have to go out and do the exploration. So a false positive is no big deal.

Notice: AI does not replace the traditional geological process of discovery; rather, it is used as an advanced tool to scan data and narrow down targets much faster. This is true for all but one of the companies I studied. The one exception still has to prove its technology.

The real risk is where the AI misses a real deposit, and for that, so far, we have no model and not enough data to make an educated guess.

Why not Equity?

Equity or ownership in the mine exposes you to a different kind of risk, like geopolitics, commodity-price fluctuations, permits, and unreliable prices over a long, extended period of time. On top of a fundamental clock mismatch between venture capital and mining.

The Demand You Bet On Can Vanish

And underneath all of that sits a deeper risk: a single technology breakthrough can cut how much of the metal the world needs.For instance the grain boundary diffusion achieves the same magnet performance with roughly a tenth of the dysprosium that conventional alloying needs. Own the ground for ten or fifteen years, and the demand you bet on can shrink before you ever sell a tonne.

Venture Capital in Two Words: Capital and Control

There's also a reason rooted in the cap table. In venture capital, every time you dilute, you give up power too, and at some point, you can be forced to exit just to return the money to your investors. That structure doesn't let you venture into a higher-risk profile. Datarock is the clearest example: its primary investor was IMDEX, which moved from a minority stake to 51% and finally bought the whole company. It exited to its own strategic investor.

Talent

They're geologists and ML scientists. Their gift is finding deposits and building models, not raising mining capital, holding tenure, permitting, or running drill programs. So they build what they know: software. The people best at finding are the least equipped to own.

So what happens if you start at group 1?

Well, it’s crowded. So you differentiate. Take a close look at this group,

They're commercially smart, but smart isn't durable. Nearly every company in group 1 has a genuinely distinct business model: 4Point's volumetric pricing plus NSR toggle, VRIFY's three-product platform, GoldSpot's royalty machine, Beholder's equity-in-lieu option. They've all clearly noticed business model matters. But a clever model is copyable.

A distinct business model is the minimum and less of a durable moat. None of it survives 15 years on its own.

But the model can be the conversion mechanism

Most capture cash (fees, SaaS revenue), but there is a ceiling. This business model monetizes the edge directly, and when the edge decays, you're done. It’s not a dead end; these companies still generate millions in revenue, return the money to investors, or they already have. But it will be harder every year.

Every durable player designed the business model as the conversion mechanism:

KoBold

intelligence-for-equity: trades algorithm output for equity in projects.

GoldSpot

Franco-Nevada with AI: built to turn AI screening into a royalty/equity book.

Lithosquare

partnership fees, NSR plus earn-in: designed to reach a royalty position without the capex.

4Point

The cash to NSR toggle: a switch designed to convert fees into ownership.

VerAI

Stake the claim first, let partners earn in: own the ground, then sell access.

What remains for the rest?

The resolution: possession is the only durable moat. Data and algorithms are reproducible or perishable. That's why KoBold's number couldn't come from the algorithms. But their business model helped them to own a significant portion of their portfolio. They have hard assets now.

Can any of the companies in layer 1 do what KoBold Metals did?

If you starve the rest, you'd better take their possession. The data KoBold trained in their algorithm is in their system. But a data advantage is only worth anything permanent if you convert it into ownership.

A handful did try to own equity and then sold it. OreFox is the clearest. Alongside its targeting software, it runs an exploration arm that pegs the ground its own AI flags, then sells it rather than keeping it: in January 2022, it pegged the Titan Gold Project in Queensland and sold it outright to Queensland Gold Hills for 300,000 shares, no royalty attached. It held the tenure just long enough to pass it on. They also have an exploration arm, OreFox Exploration, but it seems to be dormant for now. The company has scaled down the engineering team 84% in the last 6 months.

The End?

Algorithm and data are an edge, not a moat because they decay. A clever business model is necessary but copyable. The only advantage that lasts 15+ years is possession. Owning the ground or the equity and in some cases the metals (TMC). The tailwind market floats everyone for now; when it normalizes, the layer-1 vendors get absorbed, and only the asset-owners hold. KoBold proves it: the unique data and the algorithm got them in the power position, but the billion-dollar valuation came from owning Mingomba.

References

The following companies are the subject of the analysis:

MINML, 4Point AI, Mineral Forecast, Mineflow, Mineural, Exploration Machine, AVRA, Beholder, Minerva Intelligence, Datarock, Terra AI, OreFox, Geomorphic AI, RadiXplore, MinersAI, Koan Analytics, VRIFY, ExploreTech, Lithosquare, Earth AI, GoldSpot Discoveries, VerAI, KoBold Metals, Albert Mining.

Peer-reviewed literature

Chen, R., Xia, X., Tang, X., & Yan, A. (2023). Significant progress for hot-deformed Nd-Fe-B magnets: A review. Materials. https://pmc.ncbi.nlm.nih.gov/articles/PMC10343483/ [R57]

Itakura, M., Namura, M., Nishida, M., & Nakamura, H. (2020). Elemental distribution near the grain boundary in a Nd–Fe–B sintered magnet subjected to grain-boundary diffusion with Dy₂O₃. Materials Transactions, 61(3). https://www.jstage.jst.go.jp/article/matertrans/61/3/61_MT-M2019265/_html/-char/en [R58]

Government, legal & regulatory filings

Aterian plc. (2025, December 9). Transformational AI-led JV with Lithosquare SAS (RNS No. 8058K) [Regulatory announcement]. Financial Conduct Authority National Storage Mechanism. https://data.fca.org.uk/artefacts/NSM/RNS/3e41f6e5-a2ac-4516-9a79-08f71ea1a4da.html [R8]

Australian Business Register. (2026, June 17). Current details for ABN 76 636 974 420: OreFox Exploration Pty Ltd [Registry record]. Australian Government. https://abr.business.gov.au/ABN/View?abn=76636974420 [R30]

Australian Securities and Investments Commission. (2026, June 17). Organisation and business name search: ACN 636 974 420, OreFox Exploration Pty Ltd [Registry record]. https://connectonline.asic.gov.au/RegistrySearch/faces/landing/panelSearch.jspx?searchText=636974420&searchType=OrgAndBusNm [R31]

IMDEX Limited. (2026, February 2). IMDEX completes Datarock acquisition [ASX announcement]. Australian Securities Exchange. https://announcements.asx.com.au/asxpdf/20260202/pdf/06vv4712m7nlrm.pdf [R32]

Mineral Tenure Act, RSBC 1996, c 292 (current to June 9, 2026). King's Printer, Province of British Columbia. https://www.bclaws.gov.bc.ca/civix/document/id/complete/statreg/96292_01 [R1]

MINML Ltd. (2026, March 2). Return of allotment of shares (SH01): 6,250 shares allotted 26 February 2026 (Company No. 16923796) [Regulatory filing]. Companies House. https://find-and-update.company-information.service.gov.uk/company/16923796/filing-history/MzUwNzg1NTAwMmFkaXF6a2N4/document?format=pdf&download=0 [R19]

MINML Ltd. (2026, March 12). Return of allotment of shares (SH01): 625 shares allotted 6 March 2026 (Company No. 16923796) [Regulatory filing]. Companies House. [R20]

MINML Ltd. (2026, May 14). Return of allotment of shares (SH01): 3,024 shares allotted 15 April 2026 (Company No. 16923796) [Regulatory filing]. Companies House. [R21]

Queensland Gold Hills Corp. (2022, October 19). Management's discussion and analysis for the six months ended August 31, 2022 [Regulatory filing]. SEDAR. https://wp-q2metals-2023.s3.ca-central-1.amazonaws.com/media/2024/02/OZAU-MDA-Q2-August-31-2022-FINAL.pdf [R23]

VerAI Discoveries, Inc. (2022, October 31). Form D: Notice of exempt offering of securities (Series A) (Central Index Key No. 0001858880) [Regulatory filing]. U.S. Securities and Exchange Commission EDGAR. [R13]

VerAI Discoveries, Inc. (2025, February 27). Form D: Notice of exempt offering of securities (Series B) (Central Index Key No. 0001858880) [Regulatory filing]. U.S. Securities and Exchange Commission EDGAR. [R14]

Official corporate & investor communications (primary)

Eramet. (2026, June 9). Eramet, Lithosquare and BRGM combine their expertise and leverage AI to accelerate the discovery of critical metals [Press release]. https://www.eramet.com/en/news/eramet-lithosquare-and-brgm-combine-their-expertise-and-leverage-ai-to-accelerate-the-discovery-of-critical-metals/ [R9]

Queensland Gold Hills Corp. (2022, January). Queensland Gold Hills acquires 90-square-kilometre Titan Gold Project adjacent to Big Hill Gold Project [Press release]. Newsfile. https://www.newsfilecorp.com/release/111542/Queensland-Gold-Hills-Acquires-90SquareKilometre-Titan-Gold-Project-Adjacent-to-Big-Hill-Gold-Project [R24]

Tocvan Ventures Corp. (2026, March 13). Tocvan partners with VRIFY to accelerate exploration and enhance discovery potential with AI at Gran Pilar [Press release]. https://tocvan.com/news/tocvan-partners-with-vrify-to-accelerate-exploration-and-enhance-discovery-potential-with-ai-at-gran-pilar/ [R34]

VerAI Discoveries. (2023, March 2). AI-powered mineral discovery technology company VerAI raises $12M to radically improve the ability to locate concealed minerals critical for a sustainable future [Press release]. Chrysalix Venture Capital. https://www.chrysalix.com/news_insights/ai-powered-mineral-discovery-technology-company-verai-raises-12m-to-radically-improve-the-ability-to-locate-concealed-minerals-critical-for-a-sustainable-future [R11]

VRIFY Technology Inc. (2024, February 23). Client terms of service [Legal terms; effective March 1, 2024]. https://vrify.com/legal/client-terms-of-service [R37]

Journalism & named published sources

Ivanhoe Electric. (n.d.). Computational Geosciences Inc. https://ivanhoeelectric.com/technologies/computational-geosciences-inc/ [R59]

Petrone, J. (2024, September 3). No limits with e-Residency [Interview with D. Lubkin, Beholder]. e-Residency, Republic of Estonia. https://e-resident.gov.ee/blog/ [R45]

US Critical Materials to deploy AI-powered tech for rare earth exploration. (n.d.). MINING.com. https://www.mining.com/us-critical-materials-to-deploy-ai-powered-tech-for-rare-earth-exploration/ [R15]

Open APA elements to confirm before publication: R57 volume/issue/article no.; R58 page range; R13/R14 EDGAR accession no.; R15 publication date; R45 exact article URL (blog root cited).