A six-layer moat built around two blocks. Clean Input. Clean Manufacturing.

How is a clean industry a moat? It's usually a liability. Well. Not in Europe.

In 2016, the EU made a decision that changed the economics of manufacturing on the continent: it would reward clean production. Whoever could prove they were clean, traceable, and European wouldn't just win customers. Northvolt rode the wave and built a category.

They had a simple plan: Clean Input. Clean Manufacturing.

Block 1: Clean Input

Where do the energy and materials come from, and can you prove they're clean?

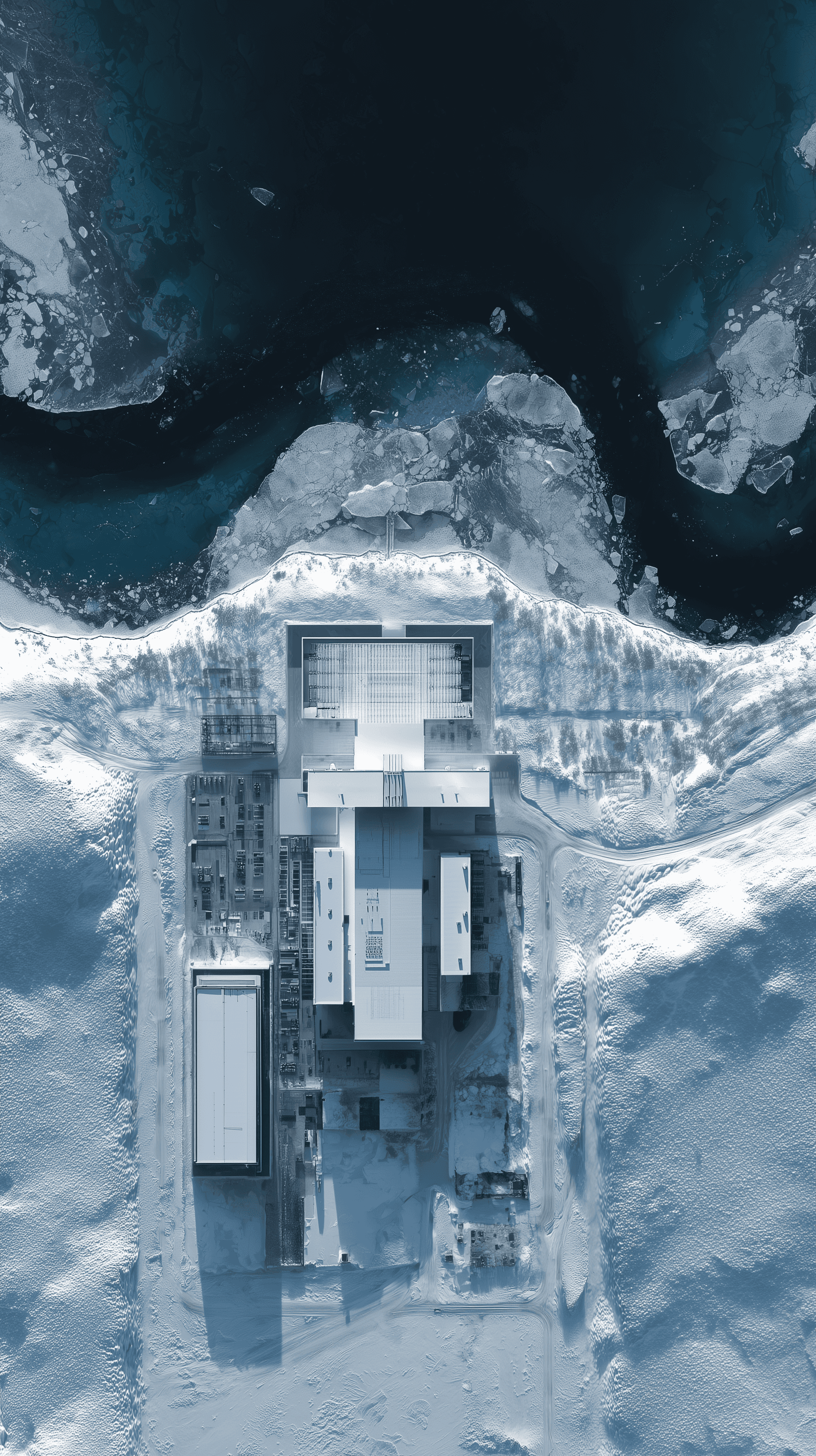

The Geographic Lock Northvolt built its Gigafactory in Skellefteå, Sweden, on top of 100% fossil-free hydro and wind power. Carbon footprint 90% lower than the industry average. No competitor could replicate that without finding an identical geography.

The Circular Supply Chain They didn't want to mine. They wanted to recycle instead. Their "Revolt" program targeted 50% of raw materials sourced from end-of-life batteries by 2030.

The Sovereign Shield Swedish government. European Investment Bank. Goldman Sachs. BlackRock. Over $8 billion deployed. Competing with Northvolt meant competing against the unified policy will of a continent. That's a structural disqualification for a rival.

Block 2: Clean Manufacturing & Downstream

Can you prove what happens inside the factory is equally defensible?

Vertical Integration as Traceability From raw cathode chemistry to finished cell, every step owned, every step traceable. When "responsibly sourced" becomes a hard requirement, full vertical control was the only way to prove it.

Customer Entanglement Volkswagen: 21% stake, €1.4 billion committed. BMW, Scania, Volvo: $50 billion in take-or-pay contracts. They didn't close deals. They built traps.

The Capital Valley of Death Gigafactories require billions spent before a profitable cell ships. That gap destroys most entrants before they start. Northvolt's scale weaponized entry cost. Any rival had to survive the same — without the sovereign backing, without the anchor customers, without the head start.

The Framework: The Regulatory Monopoly Play

Northvolt didn't invent this. The pattern underneath it is three moves, always in this order.

Move 1: Choose your legal medium

Most founders treat regulation as a constraint. It's an opportunity to innovate — regulators incentivize you and your partners; they reward you.

The EU's mandates were the architecture of the moat. They defined who could play, what counted as winning, and who was disqualified before they started. Your move: find the mandate you can build around. Compliance alone is not enough.

Move 2: Monopolize the physical input or access

Go somewhere only you can reach. Find the geography, the resource, the site with room for exactly one company — and get there first.

Northvolt found Skellefteå. KoBold Metals bought drilling records from failed mines — data no competitor can regenerate. Rocket Lab acquired Geost not for its sensors but for its US defense clearances, access that takes a decade to build. When your input is a place or a license that can't be replicated, your upstream is permanently closed.

Move 3: Lock everyone in

Make stakeholders co-owners of your position. Offtake contracts. Government backing. Supply agreements where switching is a balance sheet event, not a procurement decision.

This pattern has a past and a future.

In the past: Northvolt raised $8 billion on it. KoBold hit a $1 billion valuation without mining a ton. Rocket Lab turned a tens-of-millions acquisition into an $816 million contract.

The future is wider. The EU is expanding what counts as a strategic material. Greenland's mineral rights are a geopolitical flashpoint. The Arctic is opening. The deep sea is next. Every site that requires a permit or a sovereign partnership in a place most companies will never go is a new opening to run this play.

The regulatory medium is multiplying. The physical locations are still mostly empty.

If you're building in a regulated, physical, or resource-constrained industry and raising your first institutional round, this is the conversation I spend most of my time inside.

Have you found your Skellefteå?