The national interest required mineral resources independent of the export policies of foreign nations

For most of human history, no one owned the sea. A coastal nation ruled only as far as its cannon could fire from shore, no more than three miles. Everything beyond was the high seas. The idea called the freedom of the seas (Mare Liberum), and it held for three hundred years.

In 1945, Truman's Proclamation claimed the seabed of America's coast for the US alone, and within a few years, Chile and Peru reached out two hundred miles, and the rest of the world followed.

In 1967, a Maltese diplomat named Arvid Pardo rose at the United Nations and spoke for three hours. He called the deep seabed, beyond the reach of any flag, and named it the common heritage of mankind. His speech opened a negotiation for the Law of the Sea Treaty for decades.

In 1980, the United States, tired of waiting, wrote its own law. Congress codified it in the “Deep Seabed Hard Mineral Resources Act (DSHMRA)”.

Let’s look at the findings of the congress in June 1980 (verbatim):

The national interest required mineral resources independent of the export policies of foreign nations.

And

Pending a Law of the Sea Treaty," the uncertainty over who governed the deep sea was "likely to discourage or prevent the investments necessary to develop deep seabed mining technology.

This is the whole reason The Metal Company (TMC) and American Ocean Mineral (AOM) are abandoning the international rules and aggressively moving towards the Pacific Ocean, especially the Clarion Clipperton zone (CCZ).

Under the Act, the National Oceanic and Atmospheric Administration (NOAA) alone can grant an American company the license to:

Explore the deep seabed and the permit to mine it commercially.

In international waters. Non-US entities can at best only explore, since the International Seabed Authority (ISA) has not yet codified the laws governing collection.

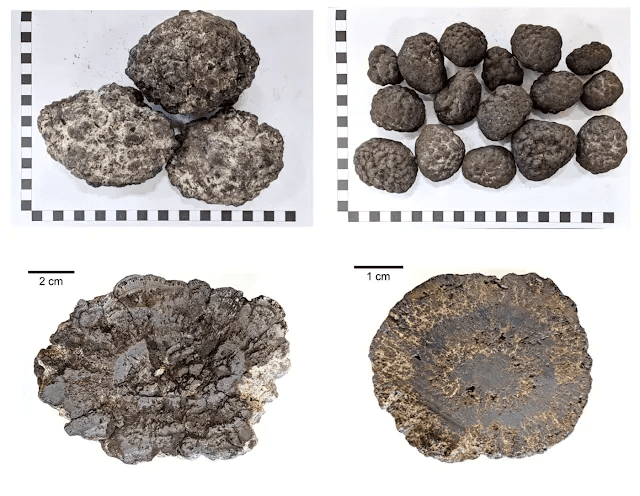

But what is in the seabed?

Polymetallic nodules are loose rocks packed with manganese, nickel, cobalt, and copper.

https://www.geologyin.com/2024/06/polymetallic-nodules.html

Two years later after DSHMRA the rest of the world wrote down the opposite conviction: the seabed is the common heritage of mankind. More than a hundred and sixty nations would come to sign but the US never ratified it.

The promise of certainty is what gave birth to the three American companies racing to the bottom of the Pacific today, TMC, AOM and Impossible Metals.

So where, exactly, is the moat?

In the value chain. The deep-sea mining value chain has three segment: permission, collection and refining.

The first link is the right to explore the seabed. This is a legal and diplomatic hurdle.

The second link is the collection and transport of the nodules. This part is an engineering challenge since the nodules are somewhere between 3 to 6 kilometers deep. Add to that an environmental challenge because marine life matters.

The third link is the refining of a wet grey stone into metal. This is the hardest of the three, because it demands both advanced chemistry and enormous physical infrastructure: plants, ports, power.

No single company independently owns all three links . Most do not even own the first one. And the first is where everything begins, because before you can lift a single nodule or refine a single gram, you have to know what is down there, and to know, you need permission.

If the metals you want lie in international waters only the International Seabed Authority (ISA) can issue you the permit.

The Authority is a body created by the world's oceans treaty and seated in Jamaica. Around 170 countries are members; the United States is not one of them. A company cannot approach it alone but it must first be sponsored by a member country, which vouches for it.ISA grants the right to explore a patch of deep seabed for fifteen years.

15 Years Is Never Enough

But that right comes with a condition designed to stop any one company from hoarding the ocean. You start with a large block of seafloor and over time, you must hand much of it back. By the third year you give up a fifth of it; by the eighth, half of it returns to the common pool.

But the US companies under DSHMRA can obtain the permit regardless of ISA approval.

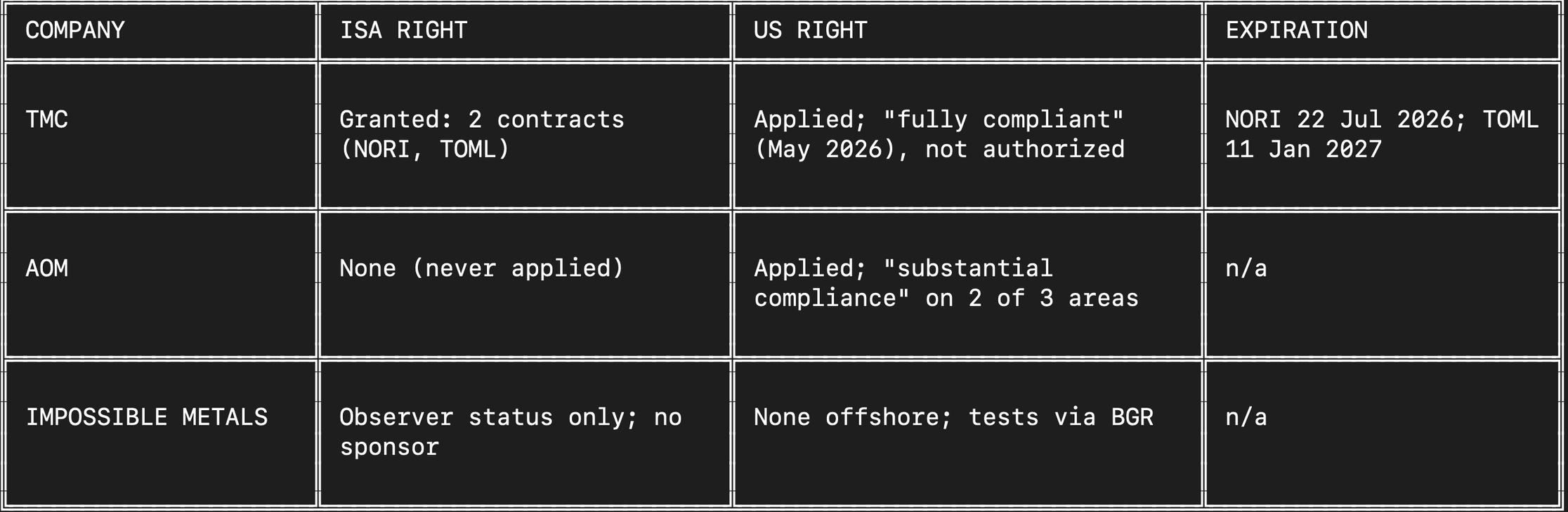

Who owns the competitive advantage?

Comparison Table

It seems TMC is ahead. Fifteen years and a billion dollars in, the world's leading deep-sea miner has explored only the NORI Area D. The rest is the largest untapped metal deposit on Earth, still mostly unexplored.

TMC seems to own a large amount of data but the other two companies can use advanced technology to survey faster. Especially AOM.

TMC also tried to obtain collection permission from ISA, but ISA failed to reach a conclusion in the 2 years window from 2023 to 2025 violating its own rules. It justifies the TMC's position to seek the alternative permission route, also known as dual permission. ISA opened a non-compliance inquiry into NORI/TOML because TMC went unilateral, and NORI's extension decision lands at July 2026 Council. TMC may lose its ISA leg as the price of the US bet.

The first layer of moat is the permit but the ISA mechanism requires the second layer for the moat. Explore quickly, keep only the richest ground.

AOM holds the fastest surveying capability of the companies in this story, because it owns the ship. While competitors charter third-party research vessels and pay by the day and lose weeks to mobilizing and integrating equipment for each campaign. AOM operates the MV Anuanua Moana, a 196-foot, purpose-built vessel kept permanently rigged for deep-sea work. That lets it survey continuously, without the start-stop of chartered fleets. The vessel consolidates the whole workstream onto one hull with permanently installed multibeam sonar, subsea tracking, a 6,000-metre-rated ROV for high-resolution imaging and sampling, and three onboard laboratories (geology, chemistry, biology) where scientists read the seafloor in real time instead of waiting to return to port.

AOM’s competitive advantage over the two and the rest of the world is the speed of exploration.

Dredge or Hover

There are really only two ways to get a nodule off the seafloor, and the three companies split between them. See the difference here.

TMC and American Ocean Minerals use the older one. A heavy tracked machine crawls the bottom, vacuums up the nodules, sediment and water, and a pump drives it several kilometres up a steel riser to a ship on the surface, which offloads to bulk carriers. It is effective and it is brutal on marine life.

One real virtue is that it works: TMC has done it, lifting three thousand tonnes from four kilometres down in 2022. AOM means to do the same but hasn't yet.

Impossible Metals built the opposite. Instead of one giant vacuum it sends down a swarm of autonomous robots that hover just above the seabed and lift nodules one at a time and keeps the cargo inside the reservoir. See the process here. There is almost no plume, and no single point of failure. On paper it is by far the cleaner method.

The green claim is worth a second look, too. Impossible Metals says it leaves 60% of the nodules in place, which sounds gentle until you read the fine print: that is 60% by count. The robots take the biggest rocks and leave the small ones, so by weight they still remove about 70% of what's down there.

So the choice on the seafloor comes down to this: the old way works and wrecks, the new way treads lightly and may never scale.

Getting the rock to shore is the easy part, and here the three barely differ. TMC and AOM both transfer their nodules at sea onto bulk carriers that steam them to port. Impossible Metals' robots surface on their own and hand their load to a passing transport ship, sparing it a dedicated support vessel.

That separation is where the whole industry stalls, and where none of the three has a finished answer. It’s beyond the scope of this analysis. The contracts are loose and we don’t have enough information to judge in 2026. But regardless of who and how the nodules get collected, the Act forces them to refine it onshore inside the US territory. All three companies have tried to complete the cycle.

Why AOM Bought a Failure

AOM and Odyssey Marine went into a reverse merger and the AOM will become a public company.

Everyone explained the AOM–Odyssey merger the same way: a quick path to a Nasdaq listing, "thirty years of deep-ocean experience," a billion-dollar critical-minerals platform. Fine. None of it explains why anyone would buy this company.

Odyssey has lost money in all but one year of its life. Its biggest win was half a million silver coins from the wreck it called Black Swan also was seized by Spain and handed back. Twenty years of going-concern warnings. AOM could have grabbed a clean shell for the listing and skipped the corpse.

Why?

Besides the obvious reasons: Odyssey already held the Cook Islands licences AOM's resource base sits on. It carried a $37 million award it had won by suing the government of Mexico over a seabed permit.

The company that had spent twenty-five years fighting sovereigns for the right to take things off the seafloor. And lost many legal battles with Spain. So AOM bought a failure, cheap, because the failure had been to the front line and come back. The entire deep-see mining is political and legal.

Conclusion

The entire industry depends on the permits, and in case the US issues unilateral commercial permits, no one knows what will happen. The strongest moat in deep-sea mining is the company that can survive the longest during legal battles while losing money year on year.

TMC is losing millions every year, still a pre-revenue company, and AOM just merged with Odyssey Marine, who knows how to survive since the 20th century, lose battles, and keep going.

Impossible Metals has the shortest head start and financial means. They are betting on compliance first and responsible recovery; it's a smart strategy to hedge against environmental backlashes, and so far we have no track record of compliance-first companies in deep-sea.

All three companies are at the edge. A very probable scenario is more mergers between two of these three companies.

References

A&O Shearman. (2026). Deep sea mining in 2026: Regulation, geopolitics, and the race for critical minerals. https://www.aoshearman.com/en/insights/deep-sea-mining-in-2026-regulation-geopolitics-and-the-race-for-critical-minerals

Alger, Neville, & Calabretta. (2026). The emerging political economy of deep-sea mining: An analysis of opaque ownership structures. Review of International Political Economy, 33(1), 193–222. https://doi.org/10.1080/09692290.2025.2553557 ⚑ add author initials

American Ocean Minerals Corporation. (2026, April 27). American Ocean Minerals announces Anuanua Moana active deployment to advance deep-sea exploration [Press release]. Business Wire. https://www.businesswire.com/news/home/20260427670998/en/

American Ocean Minerals Corporation. (2026). A merger with Odyssey Marine Exploration [Investor presentation].

Arvid Pardo: A diplomat with a mission. (n.d.). University of Malta, Open Access Repository. https://www.um.edu.mt/library/oar/bitstream/123456789/14918/1/Arvid%20Pardo%20a%20diplomat%20with%20a%20mission.pdf

British Broadcasting Corporation. (n.d.). [Audio programme w3ct5ykm]. BBC. https://www.bbc.com/audio/play/w3ct5ykm ⚑ confirm programme title

Deep Seabed Hard Mineral Resources Act of 1980, 30 U.S.C. §§ 1401–1473 (1980).

Dobush, & Warner. (2024). Deep sea mining isn't worth the risk [Finance brief]. The Ocean Foundation. ⚑ add author initials

GeologyIn. (2024, June). Polymetallic nodules. https://www.geologyin.com/2024/06/polymetallic-nodules.html

Gunasekara, O. (2025, April 29). Exploring the potential of deep-sea mining to expand American mineral production [Written testimony]. U.S. House of Representatives, Committee on Natural Resources, Subcommittee on Oversight and Investigations.

Impossible Metals. (n.d.-a). Dredging & riser systems vs. Eureka collection system [Infographic]. https://impossiblemetals.com

Impossible Metals. (n.d.-b). Eureka 3 [Interactive microsite]. https://impossiblemetals.com/wp-content/uploads/impossible-metals/eureka3/index.html

Impossible Metals. (2022). ESG annual report 2022.

Impossible Metals. (2023a). ESG annual report 2023.

Impossible Metals. (2023b). Scientific community input on Eureka II Blake Plateau testing and potential use as scientific equipment [Meeting summary].

Impossible Metals. (2024a). ESG annual report 2024.

Impossible Metals. (2024b). Myth-busting & FAQ (Version 2.3).

Impossible Metals. (2024c). Request for observer status [Submission to the International Seabed Authority, 29th session, ISBA/25/A/16].

Impossible Metals. (2025, July 15). Comment on commercial leasing for outer continental shelf minerals offshore American Samoa, request for information (Docket No. BOEM-2025-0035) [Public comment]. Bureau of Ocean Energy Management.

International Seabed Authority. (2013). Decision of the Council relating to amendments to the Regulations on Prospecting and Exploration for Polymetallic Nodules in the Area (ISBA/19/C/17).

Library of Congress. (2026). Seabed mining: Legislation and records of the 119th Congress [Search-results snapshot]. Congress.gov. https://www.congress.gov

The Metals Company Inc. (2022–2026). Annual reports (Form 10-K), fiscal years ended December 31, 2021–2025. U.S. Securities and Exchange Commission.

The Metals Company. (2025, March 27). The Metals Company to apply for permits under existing U.S. mining code for deep-sea minerals in the high seas in second quarter of 2025 [Press release]. GlobeNewswire. https://www.nasdaq.com/press-release/metals-company-apply-permits-under-existing-us-mining-code-deep-sea-minerals-high

The Metals Company. (2025, August 4). [Pre-feasibility study and world-first polymetallic nodule reserve statement] [Press release]. ⚑ confirm exact headline

The Metals Company. (2026, May 14). First quarter 2026 corporate update [Press release].

Mining.com. (2026, May 11). TMC, Allseas strike first seabed nodule mining deal. https://www.mining.com/tmc-allseas-strike-first-seabed-nodule-mining-deal/

National Academies of Sciences, Engineering, and Medicine. (n.d.). A research strategy for seabed critical mineral resources [Consensus study in progress]. https://www.nationalacademies.org/projects/DELS-OSB-24-04/event/46962

National Oceanic and Atmospheric Administration. (n.d.). Deep seabed mining. NOAA Ocean Service. https://oceanservice.noaa.gov/deep-seabed-mineral-resources/deep-seabed-mining/

Odyssey Marine Exploration. (2005–2026). Annual reports (Form 10-K), fiscal years 2005–2025. U.S. Securities and Exchange Commission.

Oxman, B. H. (2022). The fortieth anniversary of the United Nations Convention on the Law of the Sea. International Law Studies, 99, 865. ⚑ add end page

United Nations Convention on the Law of the Sea, opened for signature December 10, 1982, 1833 U.N.T.S. 397 (entered into force November 16, 1994); U.S. transmittal, Treaty Doc. No. 103-39 (1994). https://www.congress.gov/treaty-document/103rd-congress/39