When Western countries tried it, they ran into social and regulatory backlash in France and the United States. So the West made a collective decision: let China do it.

Why does China produce 70% of rare earth metals and refine almost 90% of them? Here is the short answer:

Processing REEs requires removing impurities and separating naturally co-occurring elements that are nearly identical in their chemical and physical properties. That separation process turned out to be environmentally damaging. When Western countries tried it, they ran into social and regulatory backlash in France and the United States. So the West made a collective decision: let China do it.

What has fundamentally changed?

The Paris Agreement, net zero, electrification, and increased demand for defence technologies. Although this justifies the demand, it doesn't explain why venture capital invests in this old industry. To justify the investment, investors need a vacuum.

The same regulations that drove production and processing to China didn't change in favour of traditional extraction. Instead, they turned even stricter in the West. Meanwhile, the West, especially the US, cannot remain dependent on Chinese supply. Out of all these constraints, many companies were born, but three built proprietary process technology.

MP Materials (mine-to-magnet), Phoenix Tailings a frontier technology and the UCore Metals somewhere in between.

Who invests in what company and why?

In the US, the Department of Energy, the Department of Defense, private equity firms, and public funding through IPOs are investing in MP Materials and Ucore Rare Metals.

Phoenix Tailings started like a Silicon Valley startup. Techstars and venture capital firms funded the seed and Series A rounds. Later, government grants carried them to the Series B, where they raised a significant amount. Having already demonstrated they could raise from VCs, a further DOE grant of around $66M was assigned to them last week, a signal in itself, since government grants at this stage require the company to match the award with an equivalent amount from private sources or its own capital, known as a cost-share requirement.

Why Venture Capital Invested in Phoenix Tailings?

In 2018, two MIT graduates ran a successful experiment in a backyard and took tailing waste from a mining company and separated the rare earth elements using a pyrometallurgical method.

The first sign of their competitive advantage was there from the very beginning. They were using tailing waste that no one wanted, making the input to the process extremely cheap. But it was the separation process itself that gave them their edge.

As stated in their patent, the process runs at a temperature of 270 to 320 degrees Celsius, lower than traditional methods, not the operating temperature itself, but the magnitude of reduction relative to conventional methods. A third party confirmed it in 2021, when the SBIR awarded Phoenix Tailings a $250,000 grant for the same technology.

The moat widens even more at this point. Less energy means a cleaner process, which makes permitting easier. The process also yields several metals simultaneously. That metals portfolio, combined with lower energy costs, makes them economically viable with significant margins. Large margins act as a buffer against market fluctuations. They have patented everything, which gives them an unfair advantage in squeezing more margin out of the business.

Their patent states that the input can be anything from scrap metals to mining tailings and beyond. The patent's exact language is "non-limiting," covering scrap metals, tailings, minerals, and ore. This makes their process feedstock agnostic and gives them an advantage over incumbents.

Their direct competitor is MP Materials, a mine-to-magnet company that owns the full process and holds DoD contracts. But MP Materials is dependent on the Mountain Pass mine for its input. Phoenix Tailings is not dependent on any single source.

The competitive advantage of Phoenix Tailings comes from constraints.

Lack of a Primary Mine (Resource Constraint)

Because the founders started in a backyard and did not possess a multi-billion-dollar rare earth mine. This limitation forced their platform to be "feedstock-agnostic". Because they could not rely on a consistent, uniform ore, they had to engineer a system that could dynamically process highly variable inputs.

Strict Western Regulations (Environmental Constraint).

Traditional rare earth refining generates roughly tons of highly toxic, radioactive waste for every ton of metal produced. To operate industrial refineries in heavily regulated states like Massachusetts and New Hampshire, the company was forced to completely abandon traditional solvent extraction. This regulatory reality forced them to invent a completely "closed-loop" process using selective halogenation and molten salt electrolysis that produces zero toxic byproducts or carbon emissions so they could secure operating permits.

These two factors force them to innovate, and innovation compounds over time in the form of IP.

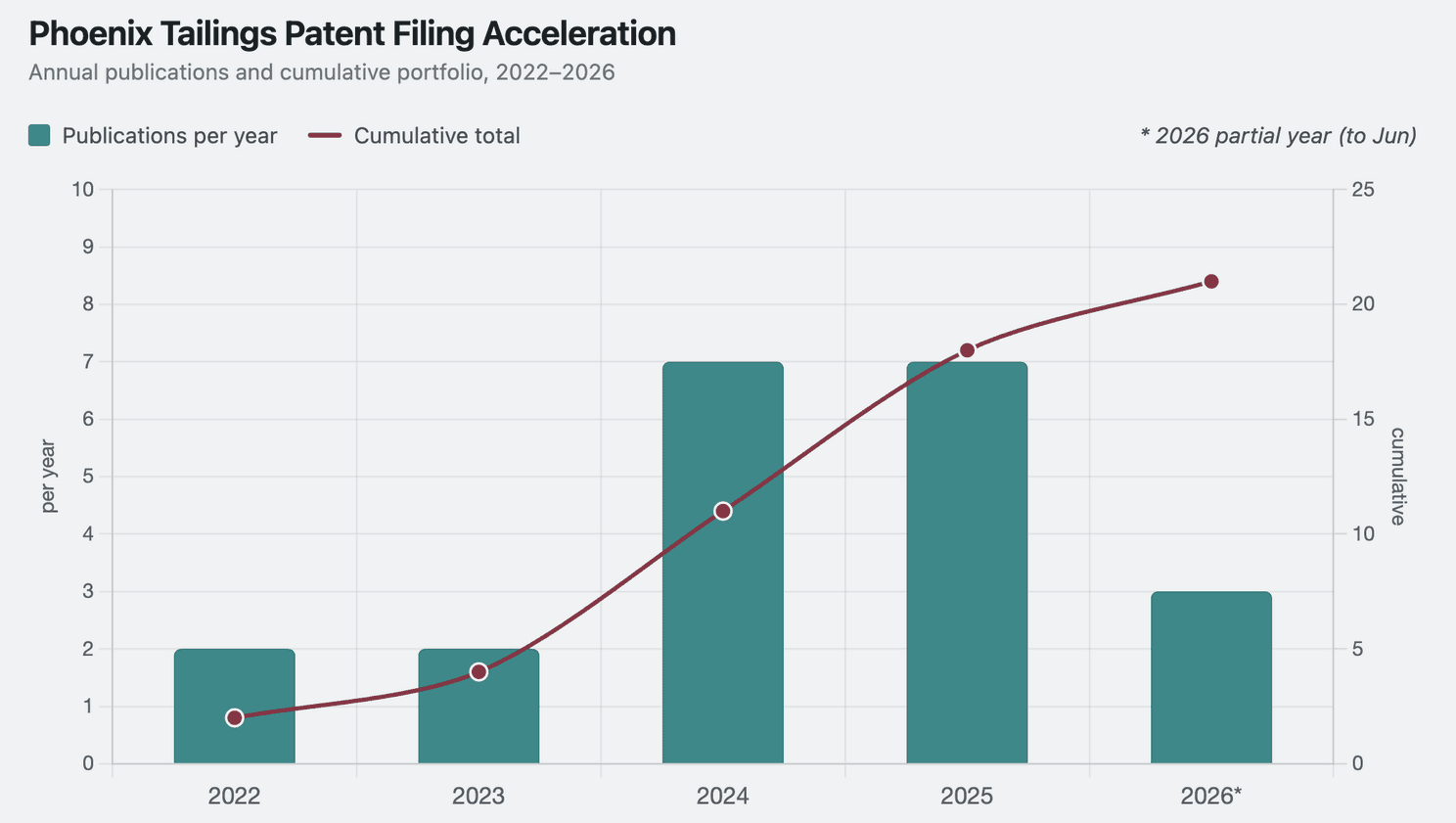

The Patent Curve

But to move the project from the labs into commercial scale, they needed automation and engineering the plants. Their patent acceleration proves they were.

Phoenix Tailings published two patents per year in 2022 and 2023. What the data does show is a change in 2024. Seven filings in a single year, more than triple the prior rate.

Why is this important?

The timing of the 2024 inflection is suggestive. The Burlington pilot facility was generating operational data around then, and real process data tends to reveal new inventions worth protecting. That's a plausible story.

Technology Validation and De-risking: The primary purpose of the Burlington facility was to test and validate the company's core electrochemical processes. By running the technology at a 40-ton pilot scale, they were able to de-risk the engineering challenges before spending tens of millions of dollars to build their massive commercial-scale plant in Exeter, New Hampshire.

Then 2025 matched that pace of patent exactly as in 2024. By the time 2026 opened, three more had already been filed with roughly half the year still to run. From zero to 21 published patents in four years, with something like 85 percent of that portfolio built in the last two years.

Patent Acceleration Curve

The investors saw a defensible company. Indeed, they later admitted it in 2025.

The lead investor in the Series A and B, Olive Tree Capital, has kept a low profile, but two other investors validate the moat.

Phoenix Tailings fills a vitally important gap in the rare earth metal production value chain. Phoenix Tailings’ non-hazardous process to refine rare earth metals from mining tailings is both economically viable and the only available process that meets US EHS requirements.

- Andrew Lackner. Managing Director of Energy Innovation Capital.

Phoenix Tailings makes rare earth metal production possible in the United States.

-Presidio Venture .

It's worth paying attention to the Presidio's funding thesis:

Presidio Ventures assists early-stage technology, internet, mobile, media, and cleantech companies looking towards global markets, like Japan and Asia, to grow their business and maintain their competitive edge.

And of course, the usual suspect, in 2025, In-Q-tell officially joined the Series B. It’s a strategic investment arm of the CIA. Their thesis is to find commercially viable tech companies that can be critical to the US defence.

Why does Phoenix Tailings think they can compete with MP Materials?

While MP Materials is the undisputed giant of the U.S. rare earth industry, Phoenix Tailings' primary defense against MP Materials is based on extreme vertical integration and "feedstock agnosticism." I see 4 reasons why they can compete against MP:

1. Feedstock Flexibility vs. Single-Mine Dependency. MP Materials is tied to the Mountain Pass mine. Because traditional chemical refineries are rigidly engineered to process a specific type of ore, any variation in the input mineralogy can severely disrupt MP's chemical separation balance. In contrast, Phoenix Tailings' electrochemical platform is completely "feedstock-agnostic".

2. The Heavy Rare Earth Advantage To make the high-performance permanent magnets required by defense systems and electric vehicles, you need "heavy" rare earth elements like dysprosium and terbium. MP Materials' Mountain Pass deposit is a "light" rare earth mine. Because of this geological limitation, MP Materials will struggle to source enough heavy rare earths natively from its own rock to make high-performance magnets. Phoenix Tailings overcomes this by sourcing diverse waste streams specifically to extract heavy rare earths, allowing them to directly produce HRREs.

3. Zero-Waste Permitting vs. Toxic Chemical Legacies MP Materials uses traditional chemical leaching and multi-stage solvent extraction. Phoenix Tailings completely bypasses toxic solvent extraction. By using selective halogenation and molten salt electrolysis in a closed-loop system.

4. Faster and Modular Deployment Because MP Materials operates an enormous, capital-intensive mega-site, its scaling efforts (like the multi-billion dollar "Project Phoenix" under previous ownership, and the current 10X downstream campus) are slow, complex engineering challenges. Phoenix Tailings' technology allows them to build automated, modular cells.

MP Materials is the direct competitor, but UCore Metals will be or …

Suppose you have unlimited funds, which of these three companies is most vulnerable to losing the competition?

UCore Metals, if they keep up with this pace

1. You Can Buy Their Entire Supply Chain Out From Under Them Because Ucore pivoted to become a pure chemical processing company, they rely entirely on third-party miners for their raw materials. Currently, every single one of Ucore's feedstock agreement non-binding Memorandums of Understanding (MOUs) or Letters of Intent (LOIs). With unlimited funds, you could approach every one of these mining projects and offer them a higher, legally binding purchase price for their ore. By outbidding Ucore, you would instantly starve their planned Louisiana facility of the materials it needs to operate, rendering their plant useless.

Meanwhile Phoenix Tailings pulled Traxys into their investors (Series B). Traxys is a major physical commodity merchant with over $10 billion in annual turnover and a deep logistics and marketing network, operating at the centre of global critical mineral markets. Much stronger partner than the partners of Ucore Metal. You do the math.

2. Their Technology is Not Chemically Unique Ucore’s core asset is its RapidSX technology, which is faster, cheaper to build, and requires a smaller physical footprint than conventional solvent extraction (CSX). However "the chemistry of RapidSX and CSX is exactly the same". Ucore is applying known chemistry more efficiently.

3. You Could Exploit Their Capital Starvation Ucore is heavily reliant on securing external funding just to build its first commercial machine, currently lacking tens of millions of dollars to complete its Louisiana complex. An attacker with infinite funds could build competing separation facilities immediately, easily beating Ucore's delayed timeline.

Ucore Rare Metals: One Layer Deep

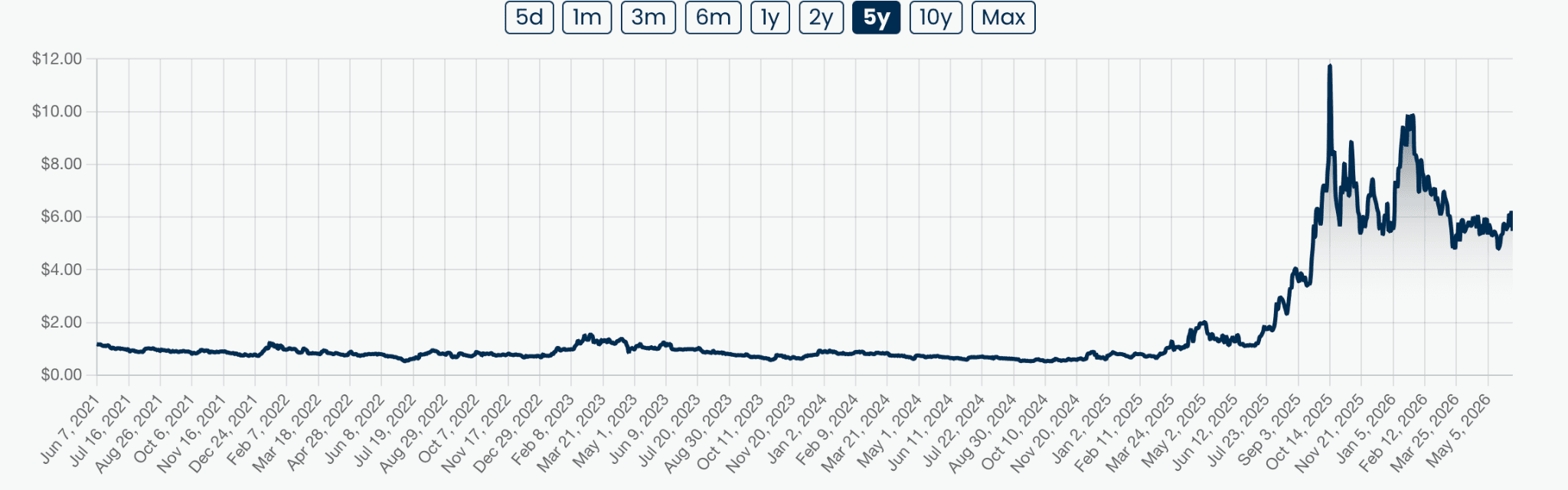

Being a public company, Ucore can leverage market sentiment by sending the right signals. The combination of government funding in 2025 and agreements increased the share price. However non-binding and LOIs gives them tools unavailable to private companies to aggressively fund the project.

Stock Price - UCore Metals Inc.

RapidSX is a novel, compact method to separate REEs. It is more efficient, faster, cheaper, and clean enough to obtain permits in North America. Whether the technology can scale remains the open question.

DoD contracts help Ucore as both investors and customers. There is a caveat: DoD requirements can change rapidly. They required Ucore to adjust RapidSX from 64 stages to 118 stages. These engineering challenges have delayed commercialisation.

On feedstock, Ucore is sourcing from Brazil rather than North American mines, suggesting their Louisiana RapidSX facility is actively testing with real-world ore. The 10-tonne shipment, at industrial rare earth carbonate concentrations, is a pilot-scale quantity not commercial throughput. It confirms the Louisiana facility is in active operation but at early-stage volumes consistent with their Phase 2 demonstration timeline.

Who wins the competition?

Rare earth minerals almost never occur in pure, standalone deposits. They are almost always mixed in with something else like iron ore, uranium, phosphate. When a mine extracts its primary product, rare earths come along for the ride as a bonus. The entire industry was built around this reality: you design the mine for the primary product and treat the rare earths as secondary recovery. Mountain Pass in California is an exception in history. The deposit where rare earths are the primary product, which allowed MP Materials to build a beneficiation process designed specifically and exclusively around rare earths from the ground up. Every other rare earth producer in the world is working within a process originally designed for something else.

MP Materials has the permits, supply contracts, and volume. They are ahead of everyone else.

Recent funding of $66M, patent acceleration, success at Burlington and the new Exeter facility in New Hampshire hint at rapid scaling. Company activity over the last three months shows a 200% increase in the business development team.

But look at 2018, when they were just starting, they were relentlessly hiring engineers. That same pattern has repeated for eight years. What venture capitalists see is a team of doers.

The real competition will be between Ucore Rare Metals and Phoenix Tailings, with the latter slightly ahead on the competitive curve. MP Materials is a mine-to-magnet company, a different category entirely.

References

Business Wire. (2026, February 24). Traxys announces strategic partnership and investment in Phoenix Tailings to strengthen US rare earth supply chain. https://www.businesswire.com/news/home/20260224716517/en/Traxys-Announces-Strategic-Partnership-and-Investment-in-Phoenix-Tailings-to-Strengthen-US-Rare-Earth-Supply-Chain

Center for Strategic and International Studies. (n.d.). Developing rare earth processing hubs: An analytical approach. https://www.csis.org/analysis/developing-rare-earth-processing-hubs-analytical-approach

Department of Energy. (n.d.). DOE's Office of Critical Minerals and Energy Innovation announces $134 million to bolster critical minerals supply chain. https://www.energy.gov/cmei/articles/does-office-critical-minerals-and-energy-innovation-announces-134-million-bolster

Department of Energy. (n.d.). Systems: How to apply for a funding opportunity announcement (FOA). https://www.energy.gov/cmei/systems/how-apply-funding-opportunity-announcement-foa

EquipmentFA. (n.d.). Machinery Partner launches capital solutions arm to streamline equipment financing. https://www.equipmentfa.com/news/39886/machinery-partner-launches-capital-solutions-arm-to-streamline-equipment-financing

Greentown Labs. (n.d.). Phoenix Tailings is building the U.S. supply chain for waste-free, net-zero rare earth metals. https://greentownlabs.com/phoenix-tailings-is-building-the-u-s-supply-chain-for-waste-free-net-zero-rare-earth-metals/

In-Q-Tel. (n.d.). IQT portfolio: Phoenix Tailings. https://www.iqt.org/portfolio?c6fb1237_page=5&company-name=phoenix+

Massachusetts Institute of Technology News. (2024, November 8). Startup Phoenix Tailings turns mining waste into critical metals. https://news.mit.edu/2024/startup-phoenix-tailings-turns-mining-waste-into-critical-metals-1108

Mining.com. (n.d.). Mountain Pass sells $20.5 million. https://www.mining.com/mountain-pass-sells-20-5-million/

Mission Matters. (n.d.). How Phoenix Tailings is transforming rare earth refining in the U.S. https://www.missionmatters.com/how-phoenix-tailings-is-transforming-rare-earth-refining-in-the-u-s

New Hampshire Public Radio. (2025, October 30). One of the country's few rare earth processing plants opens in Exeter. https://www.nhpr.org/nh-news/2025-10-30/one-of-the-countrys-few-rare-earth-processing-plants-opens-in-exeter

Phoenix Tailings. (n.d.). Press releases. https://phoenixtailings.com/press?35761714_page=1

Presidio Ventures. (n.d.). Phoenix Tailings announces investments from Presidio Ventures, EIC Rose Rock, and Envisioning Partners. https://presidio-ventures.com/phoenix-tailings-announces-investments-from-presidio-ventures-eic-rose-rock-and-envisioning-partners/

Presidio Ventures. (n.d.). News. https://presidio-ventures.com/news1/

Rare Earth Exchanges. (n.d.). Phoenix Tailings $40.2M raise: The midstream missing link gets stronger. https://rareearthexchanges.com/news/phoenix-tailings-40-2m-raise-the-midstream-missing-link-gets-stronger/

REEx [YouTube channel]. (n.d.). [Video]. https://www.youtube.com/watch?v=g7et-zyty3Q&t=85s

RePEC. (2013). [Article]. Applied Economics, 45(26), 3723–3732. https://ideas.repec.org/a/taf/applec/v45y2013i26p3723-3732.html

Small Business Innovation Research. (n.d.). Award #188367. https://www.sbir.gov/awards/188367

Small Business Innovation Research. (n.d.). Portfolio #1646735. https://www.sbir.gov/portfolio/1646735

Telluride Venture Network. (2023). TVN annual report 2022. https://tellurideventurenetwork.com/wp-content/uploads/2023/06/TVN-Annual-Report-2022.pdf

Traxys. (n.d.). Detail. https://www.traxys.com/detailnew/188

Ucore Rare Metals. (n.d.). Ucore engineering report drives optimized commercial deployment plan for Louisiana Strategic Metals Complex. https://ucore.com/ucore-engineering-report-drives-optimized-commercial-deployment-plan-for-louisiana-strategic-metals-complex/

Ucore Rare Metals. (n.d.). Ucore executes supply agreement with Critical Metals Corp. https://ucore.com/ucore-executes-supply-agreement-with-critical-metals-corp/

Ucore Rare Metals. (n.d.). Homepage. https://ucore.com/